Ask DrPeering

Ask DrPeering

Ask Dr. Peering

Dr. Peering –

What is the financial value of an Internet Exchange (IX) to its participants?

Thanks –

Stu Dent

------------

Hi Stu -

Tough question but let’s take a swing at it.

Let’s start the analysis by making a three simplifying assumptions.

First, the value an Internet Exchange point provides is facilitating the peering of traffic between participants. There are at least two dimensions to the value of peering: the value of the traffic volume peered, and the routes announced at the IX. We will only focus here on valuing the volume of traffic in this article; the routes announced deserves its own analysis.

Second, it is important to note that several large IXes have both public peering fabrics and private peering services. Private peering is traffic directly exchanged between two parties, often over a physical piece of fiber or a virtual private service. Being able to do both public and private peering represents a significant value of the IX, but unfortunately the traffic peered privately can’t be factored into the analysis since there is no visibility into the amount of traffic exchanged privately. For this reason, we will have to start out with the simplifying assumption that the value of the IX is proportional only to the value of public peering. (The LINX has migrated some large traffic flows onto private peering so as a result this analysis will consequently understate their value.)

Third, let’s assume that the alternative to peering is buying transit, so the value of the IX can be estimated to be MarketTransitPrice * VolumeOfTrafficPeered for free at the IX. Under these assumptions, if the IX went away, the community using the IX would have to exchange that traffic with their transit provider at a metered rate. We further assume that the IX peak measure approximates the 95th percentile measure upon which transit is billed.

We say ‘peered away for free’, but public peering is not completely free. The cost of public peering includes some monthly recurring costs for each participant at the IX. If we subtract these costs from the value derived, we can estimate the value of the IX to the population:

ValueIX = TrafficPeeredAtIX * TransitPrice – CostOfPeering*NumberOfMembers

Let’s plug in some public peering traffic stats (https://www.euro-ix.net/resources/list-eur.php) and AS counts (https://www.euro-ix.net/member/m/peeringmatrix) into the model and test out the formula. (Some in the Peering Community pointed out that the measurement methodologies are not consistent across IXes, so consider this simply an exercise illustration of the model.)

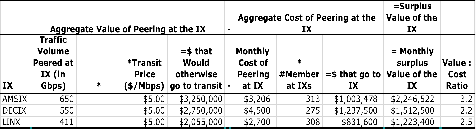

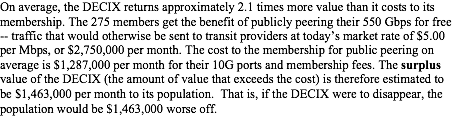

Under these assumptions, the model allows us to make the following statements about the DECIX for example:

An Internet Exchange Point facilitates the exchange of traffic between peers, using a public (shared) peering fabric like ethernet, or privately between two peers using dedicated wires or fiber.

Value of an Internet Exchange?

February 18, 2009

Simplifying Assumptions and observations surrounding the model

1) The model assumes that the next best alternative to peering at the IX is transit. However, a somewhat common next best alternative to peering with the peers at this IX, is hauling that traffic to a different IX and peering that traffic away there. This alternative peering solution may be less expensive than the transit alternative cited. The model may be over or under estimating the value of the IX.

2) We are ignoring the cost of transport (circuit) into the public peering fabric. This cost varies widely, from transoceanic builds to transcontinental circuit extensions to in building cross connects.

-

3) The cost of peering side of the equation is ignoring equipment costs. The equipment required for peering varies widely and may represent a significant capital and operational expense. With varying amortization schedules and different operational models, this is more difficult but possible to include in a slightly more complex model.

4) We are assuming that the IX member count reflects public peers at the IX. Some members may not in fact not be attached or peering on the public fabric (yet), and some may use the fabric only for testing peering volume or as a failover should another IX fail. The formula therefore underestimates the value of the IX to the population actually using the public fabric.

5) We are ignoring the value of private peering, and the value of colocation with private peers. Some IXes provide additional value by supporting private peering as well as public, so the model underestimates the value of the IX.

6) We are ignoring the marketplace effects (for example, the ability to sell services at the IX, and negotiating with many suppliers in an open market), so this model underestimates the value of the IX.

7) We are assuming that the cost of the peering fabric includes only the public peering port and any association fees. Specifically, we are ignoring colocation expenses, install fees, etc. The model may be under estimating the cost of peering and therefore over estimating the value.

8) We are assuming that traffic volumes are measuring free peering across the exchange – there may in fact be some paid peering. The traffic may not be ‘free’ peering so the model overstates the value of the IX. The model may be underestimating the value for the recipient of the paid peering revenue, and over estimating the peering value for the traffic that is not actually free.

9) We are assuming that the peak measure in+out, which is what the IXes generally report, approximates the 95th percentile that both sides of a peering relationship are saving. There are arguments that this overestimates the value of peering, since traffic in one direction is generally ‘free’, and the other is the traffic the peers would otherwise pay transit fees for. Others argue that both sides, sending and receiving are saving money in both directions to some degree, so the value of peering is actually closer to double that.

10) By averaging traffic volumes and costs, we are implicitly assuming that all ISPs peer the same amount of traffic. In reality, there will be some big winners, and some who won’t receive the ‘average’ peering benefit, so the model may be overestimating the value of the IX for the average peer.

11) We are ignoring non-recurring fees (such as install fees).

12) We are ignoring price discounts on second and subsequent ports.

Criticism of the model for the Value of an Internet Exchange.

The model is generalizing: working with averages, flattening the vast differences between networks, the alternatives available, and setting aside the many other considerations that make peering different for different peers.

The model ignores the value of unique routes, those only heard at this IX, which are inherently more valuable than those also available at alternative IXes, especially those IXes that are topologically close to the IX considered.

The ISPs that represent a large proportion of the traffic volume may not peer with the ‘average’ participant.

Acknowledgements

Thanks to Chris Park (EasyNet), Randy Epstein, Richard Steenbergen (nLayer), Joe Provo (ITA) and a handful of anonymous contributors for their critiques, corrections, and insights.

(Check out the “Modeling the Value of an Internet Exchange Point” article.)

Dr Peering

Under these assumptions, the model allows us to make the following statements about the DECIX for example:

The 2014 Internet Peering Playbook

In Print

and for the Kindle:

The PDF, ePub and

.mobi files are

also available as a

perpetually updated

DropBox share:

Price: $9.99

and in French!

The 2013 Internet Peering Playbook

also available for the Kindle:

and the ipad