LastModified: *** May 17, 2005 ***

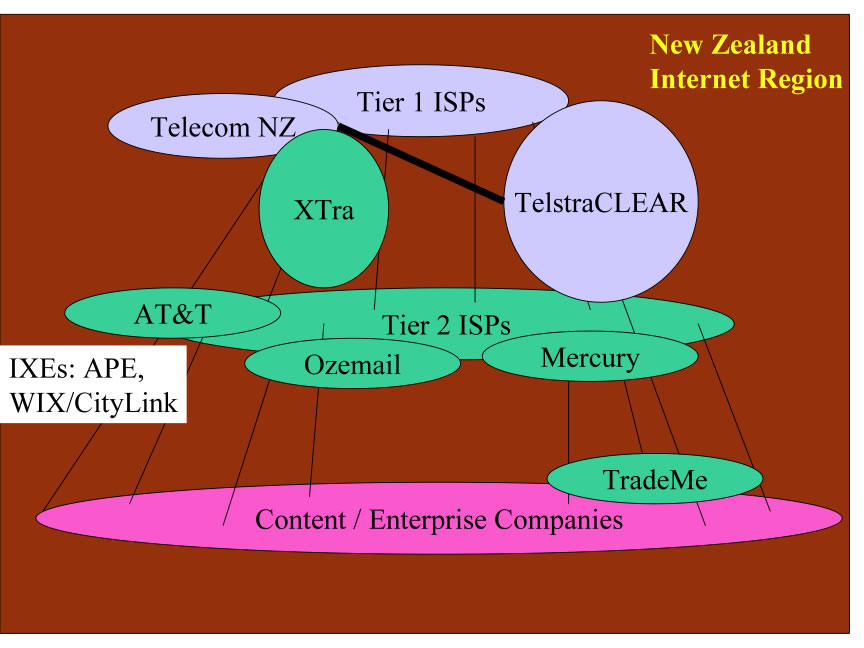

Figure 1 - Peering Ecosystem Diagram

Definitions. Within each of these Internet Peering Ecosystems we find at least three categories of players:

These rough classifications and definitions are important because they help us both

There are a couple of notable points regarding the New Zealand Peering Ecosystem.

First, today, Tier 1 ISPs are peering somewhat openly with Tier 2 ISPs in New Zealand. There are only two Tier 1 ISPs, TelstraCLEAR and Telecom New Zealand (with AS9325 is “Telecom Xtra”, the retail ISP side of TNZ, and AS4648 which is the ISP wholesale arm called “Global Gateway”). TelstraCLEAR is owned by Telstra, a Tier 1 ISP in Australia, acquired in December 2001 . However, New Zealand is the only ecosystem in which a Tier 1 (TelstraCLEAR) is peering openly with Tier 2 ISPs. They are peering at both the Auckland Peering Exchange (APE ) and the Wellington Internet Exchange (WIX ), operated over CityLink .

There is currently a massive disruption in the New Zealand Peering Ecosystem in that TelstraCLEAR has publicly announced that they will no longer peer freely. Telecom New Zealand is signaling that they will similarly tighten their selective peering policy by pulling out of the WIX. The community of ISPs that have enjoyed free access to the 30-40% of New Zealand Internet customer that Telecom New Zealand has and the 20-30% that TelstraCLEAR has , are now complaining bitterly that this represents an unfair business practice.

Secondly, CityLink has the most widely distributed exchange system that we studied. Rather than spreading the IX across 6-8 colocation sites as is common in Europe, they interconnect several hundred buildings. Of the 120 participants, only 30 or so are ISPs – the remaining are content, enterprise and government customers that are using Citylink to peer, buy transit, set up VPNs, or purchase dark fiber interconnections with ISPs. This meld of a Peering Exchange and Transit exchange, whereby customers can buy from any ISPs connected to the fabric is quite unique. Specifically, it reflects an awareness of the benefits of peering to the Content Providers that we have not seen in other ecosystems.

The Tier 1 ISPs in this Peering Ecosystem include

who collectively sell access to all routes in this ecosystem.

Content Providers peer and buy transit across CityLink for several reasons .

Each of the larger two Internet Exchanges in New Zealand carry about 500Mbps of traffic on the public LAN as of Feb 2005.

The stage for the game of chicken has been set – one side, the open peers at the WIX including TradeMe stand to lose their free peering with TelstraCLEAR eyeballs. TelstraCLEAR potentially stands to lose their free access to TradeMe content, a very popular portal.

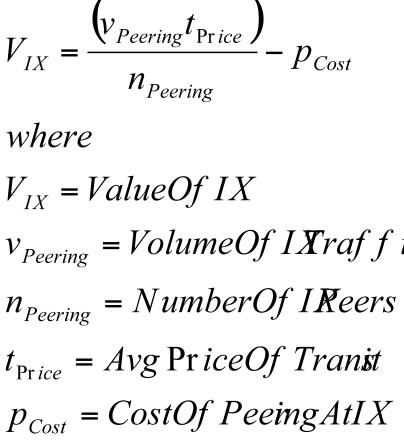

Definition: The Financial Value of an Internet Exchange is a measure of the financial value derived from an IX by its participants. It can be estimated by subtracting the collective cost of participation from the collective benefits of participation (sending that peering traffic over a transit service instead).

Let’s start the analysis by making a three simplifying assumptions.

First, the value an Internet Exchange point provides is facilitating the peering of traffic between participants. There are at least two dimensions to the value of peering: the value of the traffic volume peered, and the routes announced at the IX. We will only focus here on valuing the volume of traffic in this article; the routes announced deserves its own analysis.

Second, it is important to note that several large IXes have both public peering fabrics and private peering services. Private peering is traffic directly exchanged between two parties, often over a physical piece of fiber or a virtual private service. Being able to do both public and private peering represents a significant value of the IX, but unfortunately the traffic peered privately can’t be factored into the analysis since there is no visibility into the amount of traffic exchanged privately. For this reason, we will have to start out with the simplifying assumption that the value of the IX is proportional only to the value of public peering. (The LINX has migrated some large traffic flows onto private peering so as a result this analysis will consequently understate their value.)

Third, let’s assume that the alternative to peering is buying transit, so the value of the IX can be estimated to be

MarketTransitPrice * VolumeOfTrafficPeered

for free at the IX.

Under these assumptions, if the IX went away, the community using the IX would have to exchange that traffic with their transit provider at a metered rate. We further assume that the IX peak measure approximates the 95th percentile measure upon which transit is billed.

We say ‘peered away for free’, but public peering is not completely free. The cost of public peering includes some monthly recurring costs for each participant at the IX. If we subtract these costs from the value derived, we can estimate the value of the IX to the population:

ValueIX = TrafficPeeredAtIX * TransitPrice – CostOfPeering*NumberOfMembers

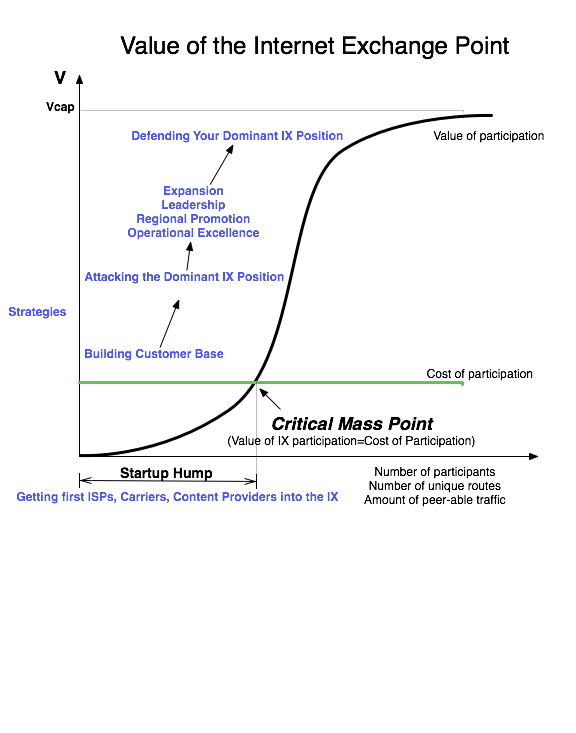

Observation: The Internet Exchange Points exhibit the characteristics of what economists call the “Network Externality Effect”; the value of the product or service is proportional to the number of users of the product or service .

Internet Exchanges are a special case of this effect; the value of an Exchange Point is not the number of participants but a slightly more complex calculation including the number and uniqueness of the routes and volume of traffic peered. Since the value of the IX to an ISP is proportional to the amount of traffic the ISP can exchange in peering relationships at the IX, the value of the IX to the peering population follows the network externality graph as shown below.

On the Y-axis we see the value of the Internet Exchange Point. On the X-axis we see the independent variable that causes the value of the IX to increase; we will use the number of participants for now; as more participants connect to the exchange for peering, the more value an NSP could derive from peering at the IX

All Internet Exchange Points go through the following growth curve. They start out with zero or a few founding ISP members, and face the challenge of attracting additional peers into a building where there are not many peers to peer with. This is the "startup hump", and solutions to this problem were shared with the author in "The Art of Peering: The IX Playbook".

Once the IX reaches critical mass, where the value of participation exceeds the cost of participation, the a well positioned IX experiences exponential growth.

Note: Some variables in this equation may be difficult to obtain.

Many Internet Exchange Points make the aggregate peering traffic volume available to the public, but some do not.

Further, private peering exchanges often utilize cross connects making it impossible to assess the total amount of traffic traversing their private exchange. This formula is therefore more accurately described as the value of a Public Internet Exchange fabric to the participants. To calculate the value of the Internet exchange, one would need to include not only the public peering fabric, but also the benefits of private peering and buying/selling transit in an environment where interconnection cross connects is less expensive than with local loops.

Be sure to chaeck out the Modeling an Internet Exchange Point for a list of the assumptions in this model.

Now we can estimate the value of the Internet Exchange Point, or at least the value of the public peering that we can measure at the Internet Exchange Point.

This Internet Peering Ecosystem has the following Internet Exchange Points:

IXRegionIntroIntro Text, where located, how many locations, stats, eventually figure out how to get traffic volume peered and calculate value.

The price of transit in this market.

Figure 4 - The Price of Internet Transit in this ecosystem

And peering vs transit spreadsheet with parameters spelled out.

Some more text where the breakeven point is.

Some more explain text. See if we need to add multiple sized pipe peering...

DrPeering.net ©2014 | Privacy Policy | Terms and Conditions | About Us | Contact Us

The 2014 Internet Peering Playbook is now available on the iPad at the Apple Store and for the Amazon Kindle. The Kindle, ePub and PDF form are also perpetually updated on the DrPeering DropBox share.